11.3 Objectives of financial management

Businesses must decide what they want to achieve – what their strategic goals are. This is how they measure their success. There are different ways to measure the financial success of a business. The first measure owners want to establish is how much profit their business is making – that is, how much revenue remains after all expenses have been paid – and represents their return on the capital they have invested in it. Any profit belongs to the owners. They can use this money for whatever purpose they wish. The owners can choose to reinvest it back into the business to help it grow and expand (this is known as retained profits as the owner is choosing to retain part of the profit back into the business) or withdraw money for their own use (this is called drawings in the balance sheet for a sole trader or partnership and dividends for a company).

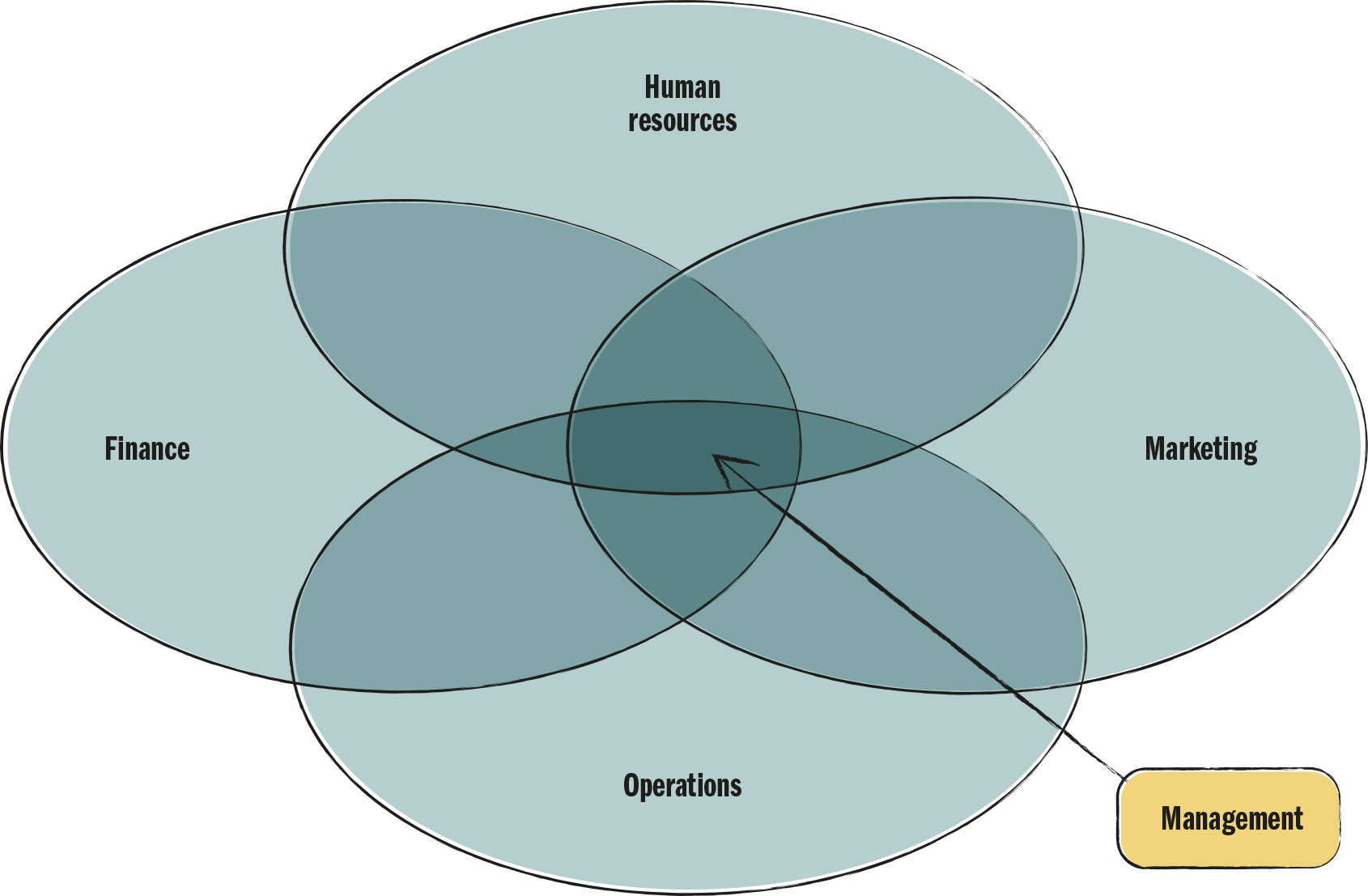

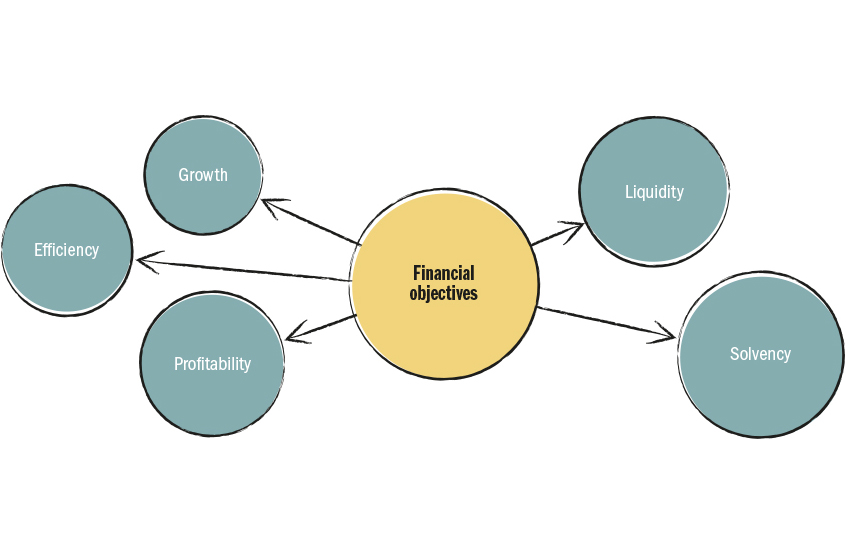

The role of financial management is to develop a tactical plan identifying short-term financial objectives and strategies that enable finance to support the whole business in achieving its strategic goals (see Sources 11.3 and 11.4). The financial manager’s objectives will include the business’s profitability, growth, efficiency, liquidity and solvency (see Sources 11.4 and 11.5). Their job will be to make short- and long-term funding decisions on debt and equity sources of funds, to develop financial policies such as cash control or borrowing and making the best use of the organisation’s scarce financial resources.

Source 11.3 Finance must support each of the other business functions. ×Source 11.3 Finance must support each of the other business functions.

Source 11.4 Financial objectives ×Source 11.4 Financial objectives

Ethical spotlight 11.1

Some objectives may conflict. For example, imagine you are the financial manager of a pharmaceutical company considering the amount of finance to provide for the trial of new drugs. How do you balance the financial needs of the company as a whole, with the fact that seriously ill people need the medicine to be available as soon as possible?

Financial reports give a detailed financial picture of the business’s profitability and financial stability. The financial manager will be able to measure the extent to which the financial objectives and financial goals of the business have been achieved. Analysis of the data will show change in the results from one year to the next, providing a trend for the business. The financial manager can use these changes and trends to determine whether the business is making more profit and is more financially stable than in the previous year.

| Objective | Definition | Data from financial reports | Analysis |

|---|---|---|---|

| Profitability | The earnings of the business after expenses have been paid | Gross profit (income statement) | Formulas are calculated as a percentage of sales. Generally, if revenue is greater than expenses, the business has made a profit. If revenue is less than expenses, then it has made a loss. |

| Net profit (income statement) | |||

| Earnings before interest and tax (EBIT) (income statement) | |||

| Efficiency | How much of total revenue is spent on expenses | Expenses (income statement) | The proportion of sales revenue that is used for expenses. |

| Growth | The size of the business compared to its competitors in the same market | Market share | Compare business sales to total market sales. The higher the percentage, the larger is their market share. |

| Number of outlets | |||

| Liquidity | The ability of the business to pay short-term liabilities using its current assets | Current assets and current liabilities (balance sheet) | Compare current assets and current liabilities. If current assets are greater than current liabilities the business has positive liquidity. If current assets are less than current liabilities it will not have enough money to pay its short-term bills as they fall due. |

| Solvency | The ability of the business to pay both short- and long-term liabilities as they fall due | Current assets, current liabilities, non-current assets and non-current liabilities (balance sheet) | Compare total assets and total liabilities. If the business is able to pay its short- and long-term debts as they fall due, it is solvent. It needs to be able to make its repayments for debt finance. |

Profitability

Profitability is the most recognisable financial objective, as nearly all businesses will seek to increase profit through increased sales and decreased costs. Owners contribute financial resources to a business when it is established and throughout the business’s lifetime. This is called capital. The return on the owners’ investment in the business is the amount of profit returned to the owners or shareholders and is expressed as a percentage of their original investment.

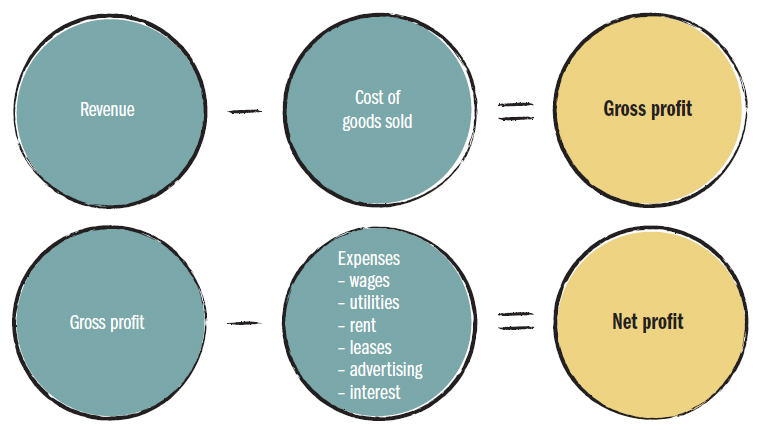

The income statement of a business (a summary of all its revenue and expenses over a period of time) will list two types of profit: gross profit and net profit.

Gross profit is the profit made on the sale of goods after paying the cost of purchasing them from the wholesaler and transporting them to the business ready for sale; that is, sales revenue minus cost of goods sold. Alternatively, it is the cost of buying the inputs that are transformed into goods for sale. The gross profit figure does not take into account any other expense, and is sometimes referred to as mark-up.

Net profit is the final amount of revenue remaining after all expenses have been paid. Source 11.6 shows how net profit is determined.

Profitability is measured using net profit. A financial manager is able to work out whether the business is making enough profit from its investment in assets by calculating and analysing the gross profit ratio and the net profit ratio. Earnings before interest and tax (EBIT) is a more precise measure of profitability than is net profit. This is because it measures the profit made directly from the operations of the business.

Owners can reinvest the profit into the business or withdraw part or all of their share of the profits from the business. For example, one owner in a partnership invested $100 000 of her money when the business was established. At the end of one year the owner receives $25 000; her return is 25 per cent. The business would be judged a success if the return was greater than the amount that could have been made from safer alternatives, such as keeping money in a savings account or investing in property.

Growth

A business that grows will increase its size and therefore its profitability in the long term. Increased output will result in more sales, which will increase revenue and therefore profit. This also depends on expenses being well managed. If a business grows too fast, it could cause liquidity or cash flow problems. Growth can be achieved by:

- increasing the physical size of the business by expanding or moving to a larger office or factory to increase operations

- increasing the value of the assets in the business; for example, by having more stock in a retail store or more equipment on a farm

- increasing sales and profits

- increasing market share through business expansion

- opening more stores, branches or offices in Australia or overseas

- taking over or purchasing a competitor

- merging with another business in the same industry

- diversifying by buying other businesses

- expanding the business’s range of products.

Business Bite

In 2009, a two-person start-up business launched a fitness product: the Fitbit Tracker. This was a small device that sensed movement, and could be clipped to a pocket. When plugged into a computer, it uploaded its information to the Fitbit website and gave the user information about the distance they had walked, calories burned, activity intensity and sleep patterns. The business grew by expanding and improving its range of products. As well as adding extra levels of tracking (e.g. heart-rate monitoring), it kept abreast of other changes in technology and the increasing public interest in fitness wearables.

In 2015 the company listed on the New York Stock Exchange, and was valued at over $4 billion. However, its value dropped in 2016, perhaps due to the fitness wearables market becoming congested, and the company has since announced that it will be expanding its focus to cover a broader ‘digital healthcare’ spectrum.

After three years of decreasing share prices, 2019 seems to be seeing a revival, especially after the company’s move into smartwatches and more competitive pricing. Some of its key products have been:

- Fitbit Ionic (September 2017) – first smartwatch

- Fitbit Versa (March 2018) – an all-day health and fitness watch

- Fitbit Ace (June 2018) – activity tracker for kids aged 8+ years

- Fitbit Charge 3 (October 2018) – swimproof, smartphone notifications, heart rate and sleep tracking and Fitbit pay.

Efficiency

Efficiency is related to profitability because a business will be able to increase its profit when it can decrease its costs. In many service-based businesses the largest expense is usually the wages and salaries of staff. In modern manufacturing businesses the largest expense will be raw materials and equipment. Efficiency may be calculated using an expense ratio, such as total expenses divided by total sales. The result is written as a percentage. The lower the result, the more efficient is the business. This means the business is able to generate more sales while spending less money.

Efficiency is also gained if a business can achieve the same level of profit from a smaller amount of inputs. For example, a small manufacturing business may have the latest equipment, allowing it to make the same level of profit as a larger manufacturer that has older, less technologically advanced equipment. In this example, the small business would be considered more efficient than the large business. Another measure of efficiency is the business’s ability to collect its accounts receivable. Many businesses sell goods and services to customers on credit to those clients with whom they have a good relationship. The customer receives a bill, or invoice, and is required to pay by a specified date, such as in 7 or 30 days’ time or at the end of the month. How long a business is given to pay will depend on the credit terms the seller allows. The accounts receivable turnover ratio calculates how many days, on average, it takes customers to pay their invoices. The shorter the average time, the more efficient the business is in collecting its accounts receivable because it is receiving money owed to it much more quickly.

Activity 11.1 Simple income statement

Income statement for Elfie’s Corner Store:

| Income | $ | $ |

|---|---|---|

| Sales | 94 500 | |

| Cost of goods sold | 58 200 | |

| Gross profit | 36 300 | |

| Expenses | ||

| Rent | 21 100 | |

| Electricity | 820 | |

| Telephone | 1100 | |

| Wages | 5200 | 28 220 |

| Net profit | 8080 | |

- Calculate the revenue that this business achieved.

- Calculate how much Elfie has paid for the inventory she actually sold.

- Deduce whether Elfie owns the premises and explain how you came to this conclusion.

- Calculate the profitability of this business. (Hint: see Source 11.6)

- Calculate the efficiency of this business. (Hint: [expenses ÷ sales] × 100)

- Discuss the profitability and efficiency of this business.

Activity 11.2 Comprehension

- Explain the impact that increasing efficiency will have on a business’s profitability.

- Analyse how sales can be used as a measure of a business’s growth.

- Identify other ways growth could be measured.

- Explain why objectives of growth and profitability may cause conflict in the short term.

Liquidity

Liquidity is a measure of how quickly a current asset including stock and accounts receivable may be converted into cash and therefore determines the ability of the business to pay short-term debts as they fall due.

Current assets are assets that are expected to be used, sold or converted to cash within 12 months, such as:

- cash in the business’s bank account, the most liquid asset

- accounts receivable, which is a relatively liquid asset as debtors are expected to pay their accounts within a short time (credit period)

- inventory, which may take some time to sell and convert to cash, making it the least liquid of the current assets

- any expenses which have been paid in advance.

Financial managers are interested in liquidity because businesses need to know how quickly they can convert an asset into cash in order to pay a liability. Current liabilities are debts that are due to be paid within 12 months. Accounts payable, bank overdrafts, short-term loans, interest payable on loans and salaries payable are all current liabilities. Liquidity provides a measure of how successfully a business manages its working capital by maintaining current assets that are greater than current liabilities, and therefore having enough short term assets to pay short-term debts as they fall due. A financial objective is to keep the business in a financially stable position in the short term by keeping it liquid.

Businesses A and B in Sources 11.8 and 11.9 illustrate the breakdown of different current assets, which is an important factor when determining liquidity.

| Current assets | $ | Current liabilities | $ |

|---|---|---|---|

| Cash | 1 000 | Bank overdraft | 1 000 |

| Inventory | 5 000 | Accounts payable | 2 000 |

| Accounts receivable | 3 000 | ||

| Prepaid expenses | 1 000 | Salaries payable | 2 000 |

| Total current assets | 10 000 | Total current liabilities | 5 000 |

| Current assets | $ | Current liabilities | $ |

|---|---|---|---|

| Cash | 4 000 | Bank overdraft | 2 000 |

| Inventory | 3 000 | Accounts payable | 3 000 |

| Accounts receivable | 3 000 | ||

| Total current assets | 10 000 | Total current liabilities | 5 000 |

Business A has twice as much finance available needed to pay all its current liabilities: $10 000 in current assets compared with only $5000 in current liabilities. However, if all suppliers have to be paid immediately the business does not have enough cash on hand to pay them.

A business that cannot pay its liabilities on time may find:

- electricity, telephone or water services are disconnected

- suppliers won’t wish to trade with it or may sell based on cash on delivery

- its credit rating may fall, which will affect its ability to obtain loans in the future

- it will incur late payment fees and increased costs

- it may have to increase long-term debt to raise cash, putting the business in a less financially stable position.

The liquidity position of business A could be improved. Examine business B and note the difference in its liquidity.

Business B has better liquidity than business A because it has more cash on hand. It has invested less money in inventory, holding a lower level of stock. Having less inventory can reduce storage costs. More money is held as available cash in the business’s bank account.

Business B can afford to pay either the bank overdraft or creditors (accounts payable) and will still have cash left over.

However, a business with very high liquidity is not more successful than one with lower liquidity. If the financial manager decides to keep a lot of cash in the business bank account, he or she will be criticised by the owners for being too cautious and not using finance effectively. Having too much cash saved is a waste of financial resources and a loss of potential profits. This cash could be put to better use in the business rather than earning a very small amount in interest from a bank.

Finally, liquidity is affected by the ability of the business to collect its accounts receivable. If the business is unable to collect these debts in a short time, it cannot convert accounts receivable to cash very quickly. Despite having a good measure of liquidity the business may find that it does not have enough physical cash to pay liabilities.

Successful financial management involves monitoring costs on a continuous basis through budgets and the control of the liquidity of the organisation to minimise the cost of having too much cash available to pay liabilities or the risk of not having enough cash to pay creditors on time. Through careful monitoring, management can calculate the amount of funds available for the day-to-day running of the business, their net working capital.

Liquidity is calculated by using the liquidity (or current) ratio. The formula is:

Liquidity ratio = Current Assets ÷ Current Liabilities

Working capital ratio = Current Assets : Current Liabilities (e.g. 2:1)

Net working capital = Current Assets − Current Liabilities

Solvency

Solvency is the ability of the business to meet its financial obligations in the long term; that is, greater than 12 months. The business is able to repay all its debt. It is a measure of whether a business is financially stable. Borrowed (debt) finance may be used to purchase expensive assets such as machinery or a factory that is needed by the business. These assets will be used to earn revenue through the production and sale of outputs and hopefully generate more than enough profit to repay the loans. As long as the business can continue to make repayments by the due date it will remain solvent and be financially secure. When interest rates on loans are low, the cost of the debt is low. Most businesses have a mixture of debt and equity financing. As loans are repaid, the ratio of debt to equity falls, reducing the level of gearing in the business. Gearing (or leverage) tells you how much debt finance the business has acquired to fund its operations compared to its level of equity finance.

Activity 11.3 Comprehension and application

- Explain how return on capital can be used as a measure of profitability.

- Imagine you are the senior financial manager of The Big Boys Clothing Company, a large retailer of street fashion clothing for 16- to 28-year-olds. Write financial objectives for this business as they should appear in the business plan. Use the SMART system:

S = specific – objectives need to have detail about what is planned to be achieved

M = measurable – the financial manager needs to be able to calculate performance and determine whether the objectives have been reached

A = achievable – it must be possible to reach the objectives given the business’s resources

R = realistic – it must be possible to reach the objectives given the business environment

T = time – a time limit needs to be set for when the objectives are to be met.

Here is an example to assist you: The Big Boys Clothing Company’s strategic goal is to achieve a net profit ratio greater than 15 per cent for the next financial year. Financial objectives could include: to eliminate bad debts and impose stricter controls on accounts receivable customers to less than 40 days and achieve a turnover rate of nine times per year. Another objective could be to introduce new technology to cut costs.

- Create financial objectives to achieve improvements in the following:

- profitability

- growth

- efficiency

- liquidity

- solvency.

- Explain why having many current assets is not a guaranteed solution to maintaining liquidity.

Short term and long term

Even though the business identifies its goals and individual department objectives, it must often prioritise them, as they may not always be able to be achieved at the same time. In fact, at times objectives, and even goals, may conflict in the short term.

A business may wish to source the cheapest funds available for the finance necessary to pursue its goals; however, these may not provide it with a long enough repayment period for financial management. A business may need its costs spread over a longer period of time for the venture to be viable.

In the short term, costs may increase and profits decrease due to a policy of growth and expansion through the introduction of new technology requiring additional debt finance. In the short term, the business will have to successfully manage its cash flow in order to make the additional repayments for the new debt. In the long term, increased sales and improved efficiency may lower overall costs and provide increased profits. Also, if goals are deemed unattainable, then some objectives may need to be eliminated or adjusted.

Overall the long term goal of financial management is to increase the wealth of the owners of the business. The strategic financial decisions may relate to expansion, takeover of another business, decreasing debt levels and so on. However, if another business goal is to be environmentally responsible, then the financial manager may not be able to choose the least expensive method of waste disposal as it would be bad for the environment. This decision conflicts with maximising profits in the short and long term. Consumers can reward businesses that use socially responsible methods of production by purchasing the products of that business. Consumers can also turn to a business’s competitors if a business is not seen to be environmentally responsible. If sales drop, so do profits. In this case, stakeholders may come into conflict and the managers will need to negotiate to achieve an acceptable result overall.

Businesses must prioritise their goals and may need to align their order of importance with the business environment and society’s values. Businesses today see the triple bottom line as a more realistic and acceptable measure of success in the long term. The triple bottom line includes:

- financial achievements such as profit levels and business growth

- social concerns through the business’s impact on people inside and outside the business, such as working conditions and contribution to the community

- effects on the natural environment; for instance, improving or at least limiting or reducing its impact such as pollution levels.